Bank Transfer Payment in Asia & Africa

A bank transfer payment allows customers to pay directly from their bank account using a local bank transfer flow. In Asia and Africa, this flow can work differently depending on the country, the local banking infrastructure, and the payment rail available.

countries:

Why offering Boost in your payment gateway?

Bank transfers in APAC & Africa

Built for e-commerce relevance

Lower risk and lower friction

Features & specifications of Bank Transfer Payment gateway

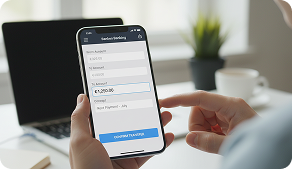

Payment flow

A typical bank transfer payment (merchant + gateway) looks like this:

Customer selects bank transfer at checkout (online bank transfer payment option)

Deposit is created via an API.

Customer completes payment through their bank flow (redirect) or through details rendered from returned metadata (OneShot).

Merchant receives status updates via the deposit status endpoint / notifications (webhooks) to confirm payment progression and completion.

Reconciliation is improved in supported setups using returned bank account details.

See how cross-border bank transfers work

Cross-border bank transfers typically introduce additional steps compared to domestic rails: compliance checks, intermediary routing (where applicable), FX handling, and different settlement windows. That is precisely why many merchants across APAC and Africa prioritize local bank transfers for domestic collection where those rails are available, then manage cross-border settlement at the PSP/acquirer layer, optimizing both conversion and operational predictability.

Want to integrate it onto your platform?

Frequently Asked Questions

How long do bank transfer payments take to settle?

What is the best way for small businesses to accept bank transfer payments?

Is bank transfer a safe payment method?

What are the key differences of bank payments by region?

Why local bank transfers outperform SWIFT in emerging markets?

Other related Payment Methods:

DANA

Alipay