FPX Payment Method

FPX payment is a Malaysia-based online banking method that lets customers pay directly from their bank accounts via internet banking authentication. It’s widely used in Malaysia for e-commerce and digital services, and it’s typically implemented as a redirect flow where customers select their bank, authenticate, and return to the merchant site for confirmation.

countries:

Why offering FPX payment in your payment gateway?

Bank-trusted payments in Malaysia

High approval, low dispute risk

Faster confirmation for fulfilment

One integration, many banks

Features & specifications of FPX payment

Payment flow

This is how the FPX Payment flow looks like:

Customer selects FPX at checkout (often labelled as “Online banking (FPX)” or “FPX payment method”).

Customer chooses their bank from the list of participating banks.

Customer is redirected to the bank’s internet banking login/authorization environment and authenticates the payment (commonly with step-up authentication such as OTP, depending on bank).

Customer receives confirmation and is typically redirected back to the merchant site/app where the order status updates.

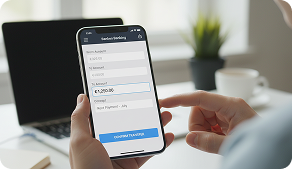

See how FPX payment works

FPX works like an online banking checkout layer: the customer selects FPX, picks their bank, authenticates within their bank’s internet banking flow, and the merchant receives an immediate confirmation to complete the purchase, making it a practical option for Malaysia-focused e-commerce where customers trust bank-authorised payments.

Frequently Asked Questions

Is FPX payment safe for online transactions in Malaysia?

FPX vs DuitNow: what are the key differences?

FPX vs credit cards: which one is better for merchants?

What are the system requirements for FPX integration?

How long does FPX settlement take for merchants?

Does FPX support recurring payments or subscriptions?

Is FPX suitable for cross-border merchants selling into Malaysia?

Other related Payment Methods:

DuitNow