QRIS Payment Method

QRIS payment (Quick Response Code Indonesian Standard) is Indonesia’s national QR code standard that enables customers to pay merchants using supported mobile banking apps and e-wallets through a single interoperable QR format. For platforms and digital businesses selling into Indonesia, QRIS is a core local payment method that supports mobile-first checkout and broad domestic acceptance.

countries:

Why offering QRIS payment in your payment gateway?

One QR, nationwide coverage

Built for mobile-first checkout

Fast confirmation, faster fulfilment

One integration, broad acceptance

Features & specifications of QRIS payment method

Payment flow

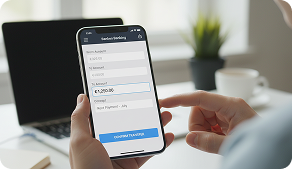

Customer selects QRIS payment at checkout.

A QR code is presented (typically merchant-presented QR).

Customer scans the QR code using a supported mobile banking or e-wallet app and authorises the payment.

Merchant receives payment confirmation and proceeds with fulfilment.

Finance teams reconcile using transaction references and settlement reporting from their PSP/acquirer.

See how the QRIS payment gateway works

A QRIS-enabled payment gateway standardises Indonesia QR acceptance by handling QR code generation/presentation, provider interoperability, and consistent payment status handling for merchants, so platforms can deploy one QRIS method across checkout surfaces while maintaining unified reporting and reconciliation outputs as volume scales.

Frequently Asked Questions

Which countries support QRIS cross-border payments?

Is QRIS payment secure against fraud and scams?

QRIS vs credit card fees: which is more cost-effective for merchants?

How long does QRIS settlement take for merchants?

How to integrate QRIS into your checkout?

What are the technical requirements for QRIS API integration?

How does QRIS compare to other Indonesian payment methods?

Other related Payment Methods:

DANA